English ![]()

Tel:

+86-13802806440

E-mail:

+86-13480210489

+86-20-31104009

+86-20-31104009

E-mail:

Views: 0 Author: Lisa Publish Time: 2025-11-11 Origin: Google

This article was originally published by WisdomTree on 30 October 2025. Written by Nitesh Shah.

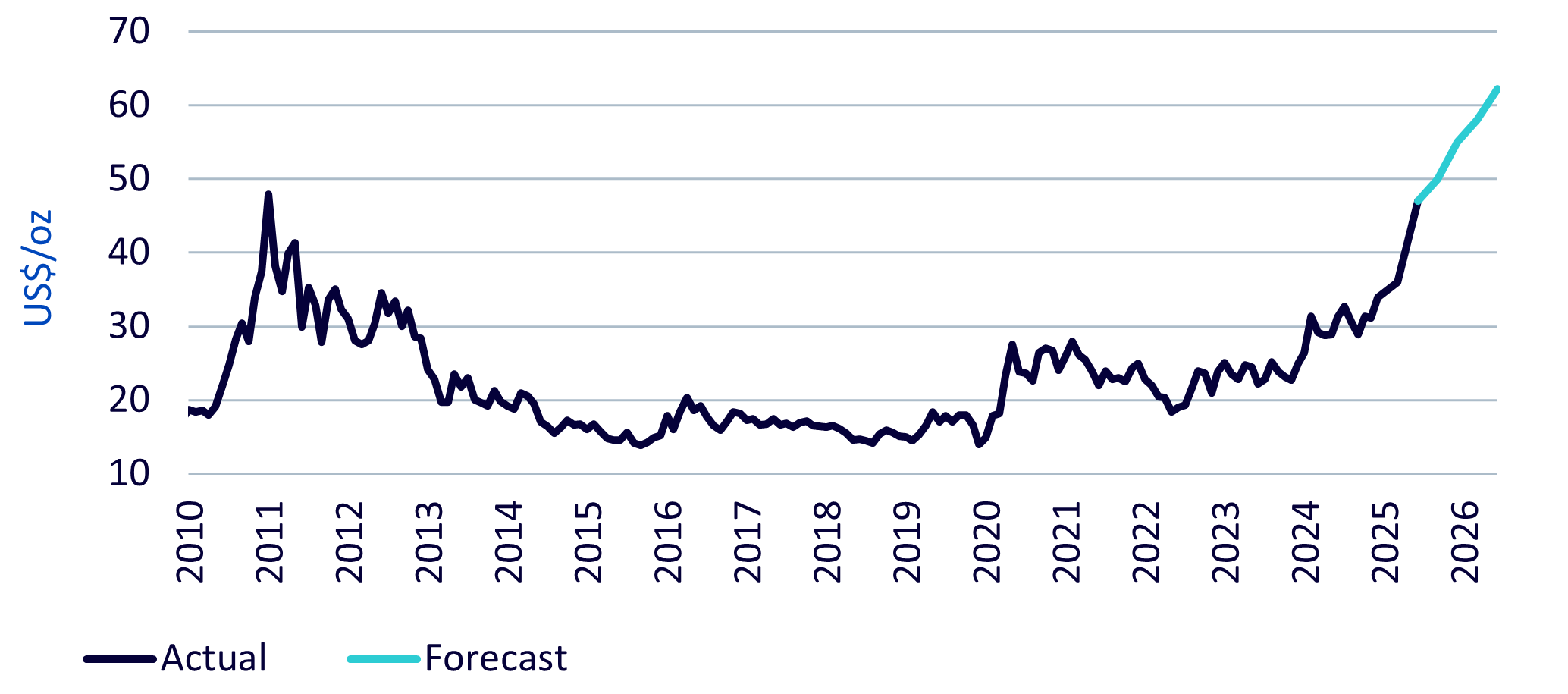

Silver prices surged to an all-time high of $53.89/oz on 16 October 2025, surpassing the previous 2011 peak. Unlike the fleeting rally of 2011, we believe today’s market is underpinned by strong fundamentals, setting the stage for further gains over the coming year.

Silver typically acts as a leveraged proxy for gold. Our models indicate a beta of 1.4 - meaning that if gold rises 1%, silver tends to climb around 1.4%, all else equal.

Gold remains well-supported by a depreciating dollar, falling bond yields, elevated inflation, and heightened policy uncertainty, particularly around trade and debt management. As we outlined in our recent Gold Outlook , gold prices are expected to reach $4,530/oz by Q3 2026 under our consensus scenario.

Using our gold-linked model, we forecast silver prices to rise to $62/oz by Q3 2026 (Figure 1), supported by robust industrial demand, even as some thrifting in photovoltaic (PV) silver usage occurs. Silver mine supply is unlikely to expand rapidly despite these price gains, as most silver is produced as a byproduct of other metals such as copper, nickel and zinc. Higher silver output will likely depend on broader strength in those base metals.

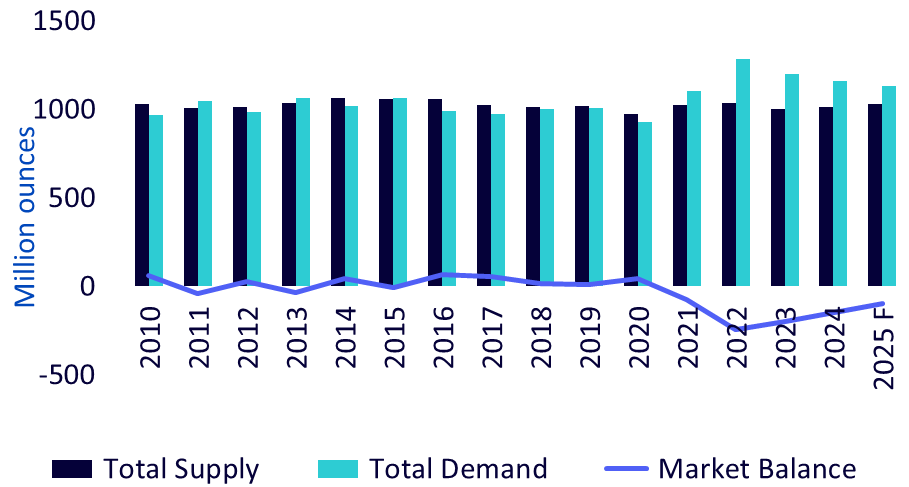

The silver market has been in deficit for four consecutive years (Figure 2), though the deficit’s size may narrow this year.

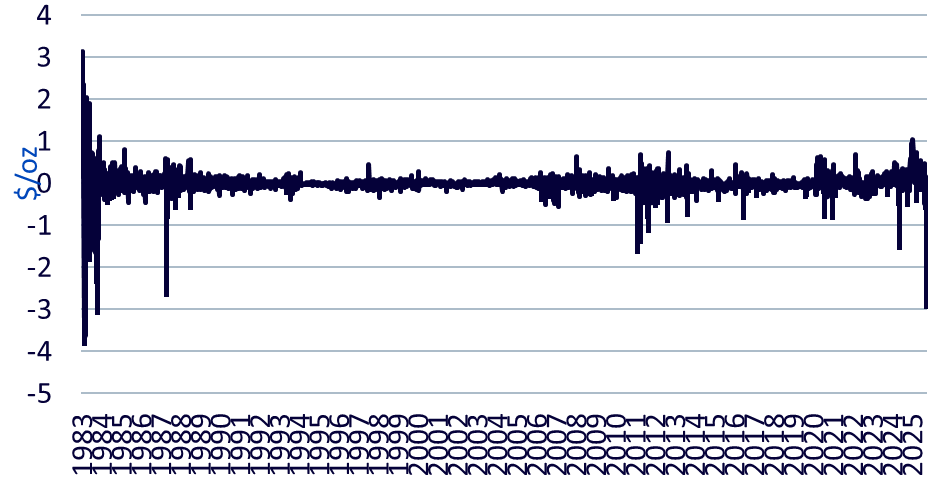

However, physical tightness has become evident in key markets, notably London and Mumbai. London spot prices are trading at a premium to front-month Comex futures (Figure 3), reaching their highest spread since the early 1980s, when the Hunt Brothers’ attempted market corner led to significant distortions.

This tightness stems partly from silver outflows from London vaults to the US, a trend amplified by fears of potential US tariffs. Traders have pre-emptively relocated metal to the US, anticipating future restrictions. The resulting wide differential between London spot and COMEX front-month prices has sparked reverse arbitrage, with silver now being air-freighted back to Europe to capitalise on price gaps. This is an extraordinary situation for this market.

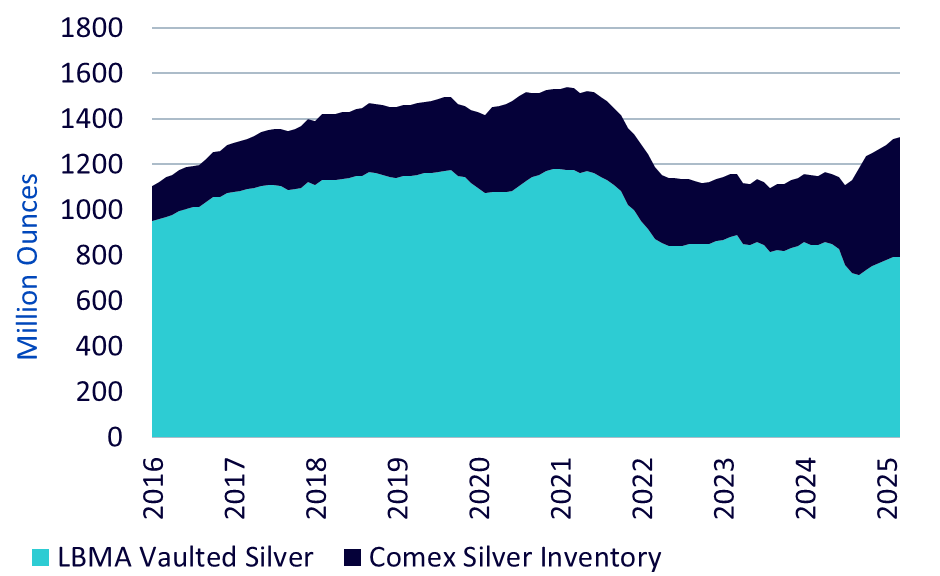

Figure 4 illustrates that the combination of London Bullion Markets Association (LBMA) and COMEX gold inventory is not necessarily low, relative to the past; it’s just that the metal is more concentrated in the US, and it has taken a spike in spot prices versus the front month future to move this metal.

As long as tariff fears persist, physical markets are likely to remain constrained. The upcoming US Geological Survey’s critical minerals list, expected in early November 2025, could be pivotal. If silver is included, it may sustain tariff speculation; if excluded, it could alleviate those concerns.

Despite reports of long queues at pawnbrokers and scrap silver buyers, much of this reflects retail investors selling silver to realise profits, rather than a surge in new buying.

We expect industrial demand to rise this year as easing monetary policy fuels greater economic activity, with Global Purchasing Managers’ Indices already surpassing the 50 demarcation of contraction and expansion (Figure 5). That should be supportive for silver demand.

Silver’s industrial demand has remained resilient in prior years despite the lacklustre broader industrial environment, largely due to its essential role in photovoltaic (PV) technologies. However, innovation within the PV industry is reshaping silver’s future usage profile.

Since 2022, manufacturers have increasingly adopted copper-cored silver pastes for heterojunction (HJT) and TOPCon cells, reducing silver content from over 50% in 2023 to just 10–15% by mid-2025, without compromising efficiency.

Further silver savings are emerging from:

Busbar-less (0BB) cell designs, cutting usage by 10–20%.

Fine-line printing and laser pattern transfer, reducing paste consumption by another 10–15%.

Laser Selective Emitter (LSE) technology, improving efficiency while optimising electrode contact.

Silver-free metallisation using copper or nickel, gaining traction in HJT and back-contact cells.

Collectively, these developments could reduce silver consumption per watt by 15–20% in 2025, marking a pivotal shift toward cost-efficient, copper-based PV production.

In India, local silver prices have approached ₹150,000/kg, yet demand has remained robust through September and early October. Premiums ranging from $0.50 to $1/oz signal strong physical buying.

Growth has been led by investment demand, with silver’s rally boosting investor confidence. Sales of bars and coins have risen, while silver ETPs continue to attract inflows, bringing loco-India holdings above 2,000 tonnes. Jewellery and silverware demand also improved ahead of the festive season, though gains were less pronounced than in investment categories.

We believe silver’s record-breaking rally is fundamentally justified, not speculative. The combination of structural industrial demand, limited supply growth, and supportive macroeconomic drivers for gold point to further upside through Q3 2026. Short-term market tightness may ease if tariff fears abate, but the medium-term trajectory remains firmly bullish.

Les informations contenues dans le site mexem.com sont données à titre d'information générale uniquement. Elles ne doivent pas être considérées comme des conseils en matière d'investissement. Investir dans des actions comporte des risques. Les performances passées d'une action ne sont pas un indicateur fiable de ses performances futures. Consultez toujours un conseiller financier ou des sources fiables avant de prendre toute décision d'investissement.